When Sarah and Michael welcomed their first child, Emma, their priorities shifted dramatically. “We went from thinking we had all the time in the world to realizing we needed to protect Emma immediately,” Sarah recalls. “The thought of something happening to both of us and leaving Emma without proper care or financial security kept us awake at night.”

Like many young parents, Sarah and Michael discovered that having children creates urgent estate planning needs that can’t be postponed. Young families face unique challenges: limited assets, tight budgets, and the critical need to name guardians for minor children.

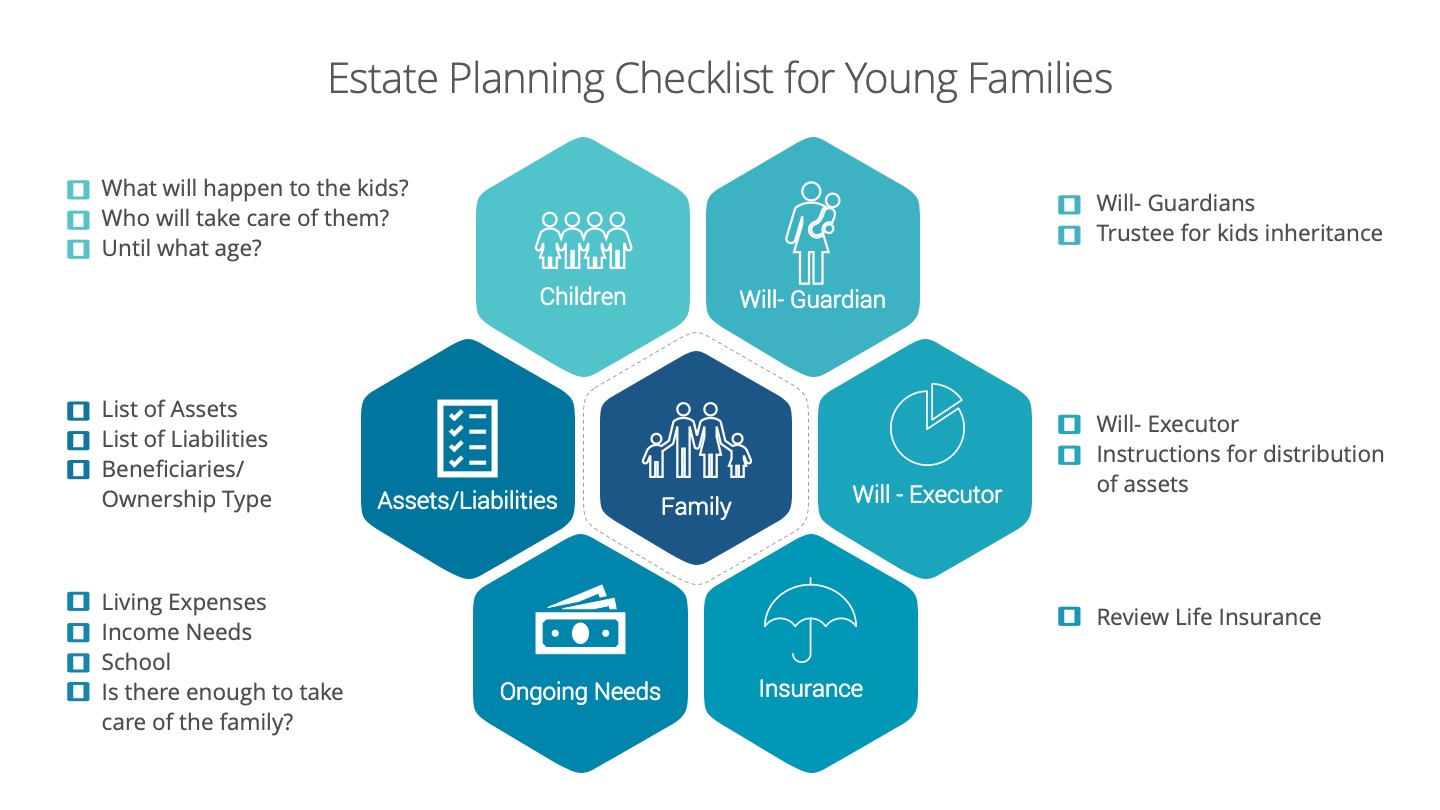

Estate planning for young families isn’t about having millions of dollars—it’s about ensuring your children are protected, cared for, and financially secure if the unthinkable happens.

Why Young Families Need Estate Planning Now

The Guardian Appointment Crisis

Without proper planning, courts decide who raises your children:

Court-appointed guardianship process:

– Judge selects guardian from available family members

– No input from deceased parents

– Potential family conflicts and disputes

– Lengthy court proceedings while children wait

– Possible placement with unsuitable relatives

Example: Tom and Lisa died in a car accident without naming guardians for their two young children. The court had to choose between Tom’s elderly parents and Lisa’s sister who lived across the country. The decision took six months, during which the children lived in temporary foster care.

Financial Protection Gaps

Young families often underestimate financial needs:

Immediate expenses after parent’s death:

– Funeral and burial costs ($7,000-$15,000)

– Outstanding debts and final expenses

– Childcare costs for surviving spouse

– Lost income replacement needs

Long-term financial needs:

– Children’s education expenses

– Healthcare costs not covered by insurance

– Housing and living expenses

– Extracurricular activities and opportunities

The “We Don’t Have Enough Assets” Myth

Common misconceptions about estate planning:

– “We don’t own enough to need estate planning”

– “Estate planning is only for wealthy people”

– “We’re too young to worry about this now”

– “Life insurance is enough protection”

Reality: Every family with minor children needs basic estate planning, regardless of asset level.

Essential Estate Planning Documents for Young Families

Last Will and Testament

Critical provisions for parents:

Guardian nominations:

– Primary guardian for minor children

– Alternate guardians if primary unavailable

– Separate guardians for person vs. property (if desired)

– Specific instructions for children’s care

Property guardians:

– Financial management for inherited assets

– Investment guidelines and restrictions

– Distribution schedules for children

– Coordination with trust provisions

North Carolina requirements (N.C. Gen. Stat. § 31-3.3):

– Written document signed by testator

– Two competent witnesses required

– Self-proving affidavit recommended

– Testator must be 18+ and of sound mind

South Carolina requirements (S.C. Code § 62-2-502):

– Written and signed by testator

– Two witnesses required

– No holographic wills recognized

– Self-proving affidavit expedites probate

Revocable Living Trust

Benefits for young families:

Avoid probate for trust assets

Immediate management if parents incapacitated

Privacy protection for family finances

Successor trustee management for children

Detailed instructions for asset distribution

Trust provisions for children:

– Age-based distributions (e.g., 25%, 50%, 100% at ages 25, 30, 35)

– Education incentives and support

– Health and emergency provisions

– Trustee discretion for special circumstances

Financial Powers of Attorney

Immediate financial management:

– Bank account access and management

– Bill payment and debt management

– Insurance claims and benefits

– Investment decisions and asset protection

– Tax filing and compliance

Durable power remains effective during incapacity

Immediate effectiveness vs. springing powers

Successor agents if primary unavailable

Healthcare Powers of Attorney and Living Wills

Medical decision-making for incapacitated parents

Treatment preferences and end-of-life wishes

HIPAA authorizations for medical information

Coordination with spouse and family members

Guardianship Planning: Your Most Important Decision

Choosing the Right Guardian

Factors to consider:

Personal qualities:

– Shared values and parenting philosophy

– Emotional stability and maturity

– Commitment to your children’s wellbeing

– Ability to provide love and guidance

Practical considerations:

– Financial stability and resources

– Geographic location and stability

– Age and health status

– Existing family size and dynamics

– Career flexibility and availability

Relationship factors:

– Existing relationship with your children

– Willingness to serve as guardian

– Support from their spouse/family

– Long-term commitment to role

Guardian vs. Property Guardian

Separate appointments may be appropriate:

Guardian of the person:

– Physical custody and daily care

– Educational decisions and school choice

– Medical care and healthcare decisions

– Religious and moral guidance

Guardian of the property:

– Financial management of inherited assets

– Investment decisions and asset protection

– Distribution decisions for children’s needs

– Court reporting and accountability

Example: Jennifer named her sister as guardian of her children but appointed a professional trustee to manage the life insurance proceeds and investment accounts.

Naming Alternate Guardians

Multiple backup options essential:

– Second choice if primary guardian unavailable

– Third choice for additional security

– Different circumstances may require different guardians

– Regular updates as situations change

Guardian Instructions and Guidance

Detailed guidance for appointed guardians:

Educational preferences:

– School choice and educational philosophy

– Extracurricular activities and interests

– College planning and expectations

– Special needs or learning considerations

Religious and cultural guidance:

– Religious upbringing and practices

– Cultural traditions and values

– Community involvement and connections

– Holiday and family traditions

Practical instructions:

– Medical history and healthcare providers

– Allergies and dietary restrictions

– Behavioral guidance and discipline approaches

– Relationships with extended family

Life Insurance: The Foundation of Young Family Protection

Determining Life Insurance Needs

Income replacement calculation:

– Current annual income × 10-15 years

– Mortgage and debt payoff needs

– Children’s education costs

– Final expenses and estate costs

Example calculation for family earning $75,000:

– Income replacement: $750,000-$1,125,000

– Mortgage payoff: $200,000

– Education costs: $100,000 per child

– Final expenses: $25,000

– Total need: $1,175,000-$1,450,000

Types of Life Insurance for Young Families

Term life insurance:

– Lower premiums for young, healthy parents

– Level premiums for 20-30 year terms

– Convertible options to permanent insurance

– Decreasing needs as children become independent

Permanent life insurance:

– Lifetime coverage with cash value

– Higher premiums but guaranteed coverage

– Investment component for wealth building

– Estate planning benefits for larger estates

Life Insurance Trust Planning

Irrevocable Life Insurance Trust (ILIT):

– Estate tax avoidance for larger policies

– Asset protection from creditors

– Professional management of proceeds

– Structured distributions to children

Trust provisions:

– Trustee selection and successor trustees

– Distribution standards for beneficiaries

– Investment guidelines and restrictions

– Coordination with other estate planning

Trust Planning for Children’s Inheritances

Age-Based Distribution Schedules

Common distribution patterns:

Conservative approach:

– Income only until age 25

– 1/3 of principal at age 25

– 1/2 of remaining at age 30

– Balance at age 35

Moderate approach:

– 25% at age 25

– 50% at age 30

– 100% at age 35

Aggressive approach:

– 50% at age 25

– 100% at age 30

Education Incentives and Support

Educational provisions:

– Unlimited distributions for education expenses

– Tuition, room, and board coverage

– Graduate school and professional training

– Educational achievement bonuses

– Study abroad and special programs

Health and Emergency Provisions

Broad discretionary authority for:

– Medical and dental expenses

– Mental health and counseling

– Emergency situations and urgent needs

– Special circumstances and opportunities

Trustee Selection for Children’s Trusts

Professional trustees:

– Investment expertise and management

– Objective decision-making

– Continuity and stability

– Regulatory oversight and accountability

Family trustees:

– Personal knowledge of children

– Emotional investment in their success

– Lower costs and fees

– Flexibility and responsiveness

Co-trustee arrangements:

– Professional and family trustee combination

– Shared responsibilities and oversight

– Balance of expertise and personal knowledge

Education Funding Strategies

529 Education Savings Plans

Tax-advantaged education savings:

– Tax-free growth and distributions

– State tax deductions (varies by state)

– Flexible beneficiary changes

– High contribution limits

2025 contribution limits:

– Annual gift tax exclusion: $19,000 per beneficiary

– Five-year bunching: $95,000 per beneficiary

– Lifetime limits vary by state ($300,000-$500,000+)

Coverdell Education Savings Accounts

Additional education funding option:

– $2,000 annual contribution limit

– Tax-free growth and distributions

– K-12 and college expenses

– Income limitations for contributors

Trust-Based Education Funding

Education provisions in family trusts:

– Unlimited distributions for qualified expenses

– Trustee discretion for educational opportunities

– Coordination with other funding sources

– Protection from beneficiary misuse

Special Considerations for Young Families

Blended Family Planning

Stepchildren and biological children:

– Clear inheritance intentions

– Guardian nominations for each child

– Coordination with ex-spouses

– Life insurance beneficiary planning

Single Parent Planning

Enhanced planning needs:

– Detailed guardian instructions

– Financial management provisions

– Extended family coordination

– Emergency planning for temporary care

Military Family Considerations

Unique planning needs:

– Deployment and geographic mobility

– SGLI life insurance coordination

– Military benefits and survivor benefits

– Guardian selection across state lines

Business Owner Families

Business succession planning:

– Buy-sell agreements and valuation

– Key person life insurance

– Business continuation for family

– Liquidity planning for estate taxes

Common Young Family Planning Mistakes

Procrastination and Delay

“We’ll do it when we have more money”

“We’re too young to worry about this”

“We’ll get to it eventually”

“It’s too complicated right now”

Reality: Basic estate planning can be completed affordably and should be prioritized immediately after children are born.

Inadequate Life Insurance

Underestimating financial needs

Relying only on employer coverage

Failing to update beneficiaries

Not considering inflation and future needs

Poor Guardian Selection

Choosing guardians without discussion

Failing to name alternates

Not providing detailed instructions

Ignoring practical considerations

Incomplete Planning

Having wills but no trusts

Forgetting to update beneficiaries

Not coordinating all documents

Failing to communicate plans to family

Taking Action: Your Young Family Planning Checklist

Estate planning for young families doesn’t have to be overwhelming or expensive. Start with the basics and build a comprehensive plan over time as your family grows and your assets increase.

Immediate priorities:

1. Draft basic wills with guardian nominations

2. Obtain adequate life insurance coverage

3. Create financial and healthcare powers of attorney

4. Update all beneficiary designations

Next steps:

1. Consider revocable living trust for asset management

2. Plan education funding strategies

3. Review and update plans annually

4. Communicate plans with chosen guardians

Don’t let the perfect be the enemy of the good. Having basic estate planning documents in place immediately is far better than waiting for the “perfect” plan that never gets completed.

Schedule a consultation with an experienced estate planning attorney who understands the unique needs of young families. Your children’s security and your peace of mind are worth the investment in proper planning.

This article provides general information about estate planning for young families and should not be considered specific legal advice. Estate planning laws vary by state and individual circumstances. Always consult with qualified professionals for advice specific to your situation.